In Focus/ European Football Finance Five-Year Overview & Trends

Recently released Deloitte’s Annual Review of Football Finance edition reveals that European football market touched €38bn aggregate revenues in 23/24, out of which, the contributing share of ‘big five’ leagues is €20.4bn, that is 54% of the total.

Looking back at the revenue performance in the European market over the last five years, from 19/20 till 23/24, some interesting insights were noticed:

– European football market has been growing at a CAGR 9% and an absolute growth of 51% over 19/20.

– The ‘big five’ leagues have been growing at 6% CAGR, lower than the overall European CAGR. In 19/20, the five leagues combined used to contribute 60% of the total revenue which, ironically, dropped to a contributing share of 54% in 23/24.

– So, who’s growing faster than the European market as a whole? Surprisingly, it’s the category of National Associations who have been growing at a much faster 23% CAGR and contributes 14% in 23/24 total revenue rising from a contributing share of 8% in 19/20. A large part of this growth can be attributed to the UEFA revenue share from participating in the UEFA Europa League & UEFA Conference League etc.

That said, the financial might and revenue generating capability of the ‘big five’ leagues towers over the others in European football. It remains a challenge to make it a more level playing field. In this blog, we will look at the financial overview and trends of the ‘big five’ league growth over the last five years, from 19/20 to 23/24.

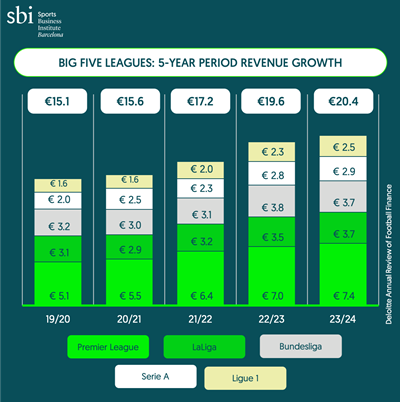

Revenue Growth by League

As mentioned above, the cumulative revenue generated by ‘big five’ league clubs have been growing at a CAGR of 6% to reach €20.4bn in 23/24, a jump of 35% from the 19/20 revenue figures of €15.2bn.

The growth is led by the Premier League, Serie A and unexpectedly, Ligue 1 clubs, who have managed to grow by 43%, 42% and 60% respectively over their 19/20 figures. However, LaLiga and Bundesliga clubs have grown at a rate slower than the median growth rate of the group:

The revenue contribution share by league has seen some interesting developments. As expected, the share of aggregate Premier League clubs has increased from 34% in 19/20 to 36% in 23/24 while at the same time, contributing shares from LaLiga and Bundesliga club revenues have decreased from 21% each in 19/20 to 18% and 19% respectively in 23/24. Revenue share of Serie A clubs remains constant at 14% and that of Ligue 1 clubs have increased by 2 percentage points.

The faster growth of revenue in case of Premier League clubs can be attributed to a combination of factors including increased matchday ticket prices, higher broadcast media rights value, a strong commercial revenue growth and increased participation in UEFA competitions leading to higher revenue in each of the three revenue streams. For Ligue 1, sustained player sales and increased UEFA revenue as a result of participation in UEFA competitions contribute fairly to the growth. Laliga, Bundesliga and Serie A clubs have borne the brunt of decreased broadcast revenue and lesser participation in UEFA competitions.

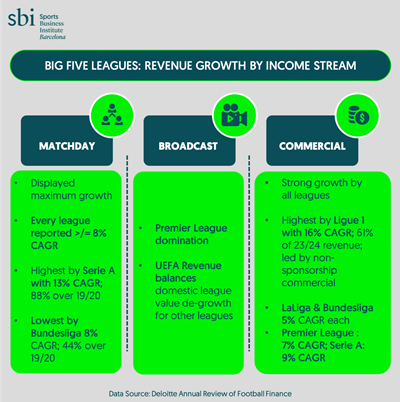

Growth by Revenue Stream

The 23/24 revenue accumulated by the ‘big five’ leagues are a complete overhaul of the situation in pre-pandemic period of 19/20. Except for the broadcast revenue, where Premier League is strongly ahead in value terms as well as growing at a significant CAGR, every member of the ‘big five’ leagues demonstrate growth in the matchday and commercial income streams. Our previous blog on media rights landscape lends a detailed perspective in this, read here

Every league displays a greater than or at least 8% CAGR (since 19/20) in case of matchday revenue stream, highest by Serie A with a 13% CAGR and in 23/24 displays 88% growth over 19/20. The lowest is reported by Bundesliga at 8% CAGR and 44% growth over 19/20 revenue figures. The growth in matchday revenue can be attributed to:

– Increased matchday fixtures with the addition of European competitions.

– Increased ticket prices added to the revenue albeit it has led to high negative sentiments from fans

The commercial revenue stream has been growing from strength-to-strength for all the ‘big five’ leagues. Not only does Ligue 1 report highest rate of growth at 16% CAGR over a five-year period it also accounts for almost 61% of the total revenue in 23/24. The growth rates for other leagues:

– Premier League – 7% CAGR

– LaLiga & Bundesliga – 5% CAGR each

– Serie A – 9% CAGR

In many cases, stadium development by clubs added to a higher revenue collection with non-football events and hospitality in the non-sponsorship based commercial revenue.

The other characteristics of commercial revenue stream can be summed up as:

– Increased appeal of Premier League sponsorship as a strong marketing tool leading to multiple high-value deals in key assets like front-of-shirt and kits. As the ban on gambling sponsorship for front-of-shirt is about to take place, we can see a renewed vigour in value growth.

– Return of crypto sponsorships, in a new and long-term strategic manner.

– Continued focus of domestic sponsors in case or Bundesliga and LaLiga adding significant value.

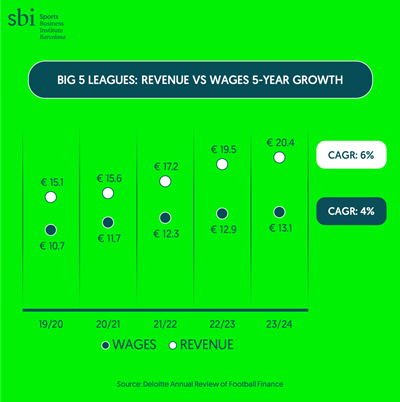

Wages

The higher rate of growth in revenues has been successful in containing the coveted wages-to-revenue (W/R) ratio, a key indicator of financial sustainability, to a large extent. A CAGR growth comparison between revenue and corresponding wages shows the control:

W/R ratio over a five-year period was seen to be the most stable in case of German Bundesliga who have been consistently in the range of 56% to 58%, much below the recommended 70% mark. The same was most volatile in case of Ligue 1 who were 89% ratio in 19/20 rising to 98% in pandemic year before gradually getting down to a more manageable 73% in 23/24.

However, the coming season scheduled to be dominated by a lower broadcast revenue figure might just put the ratio spotlight back on them. The other high spending Premier League W/R ratio seems to be settling down to a much improved 64% in 23/24 due to an increased revenue collection from the 73% mark seen in 19/20.

In Conclusion

European football is perhaps at an inflection-point period. With a plateauing or in some cases down-trending of media rights value and the entry of direct-to-consumer (DTC) model waiting to come on board, the broadcast revenue will shake up. The emphasis thus comes on commercial and matchday revenue streams to bolster the revenue figures.

Governing multi-club ownership models as well as a constant need of additional competitions to increase revenue would be the buzzwords in the near future.